The Benefits of the Three-Bucket Retirement Income Strategy

After decades of saving for retirement, the time comes for a family to actually retire. This happy transition should be simple, but more than half of all Americans worry about financial stability in retirement (according to Market Watch).

A third of our clients have already retired and live off regular withdrawals from their portfolios. Once the client and our advisors calculate the cost of supporting their lifestyle in retirement, we set up a monthly draw from clients’ investment portfolios and deposit those funds directly into their checking accounts as a replacement paycheck.

Our clients can draw conservatively 4%/year, 5% aggressively/year from their portfolios and never run out of money under any scenarios short of a nuclear war, meteor strike, or worldwide zombie apocalypse. A family with a $2 million portfolio can withdraw $80-$100,000/year, with additional funds coming from Social Security and a pension, if any.

In more than 25 years of running Heron Wealth, we have never once reduced a client’s monthly draw because of stock market volatility.

How is this possible? Back in 2009, the stock market fell 55% in six months. In early 2020, the stock market fell 35% in three months. At least once every three years, the market falls 10%; every five years or so, the market falls 20%.

Through all that volatility, we employ a straightforward solution to keep our retired clients’ draws stable and portfolios intact – the Three-Bucket Retirement Income Strategy

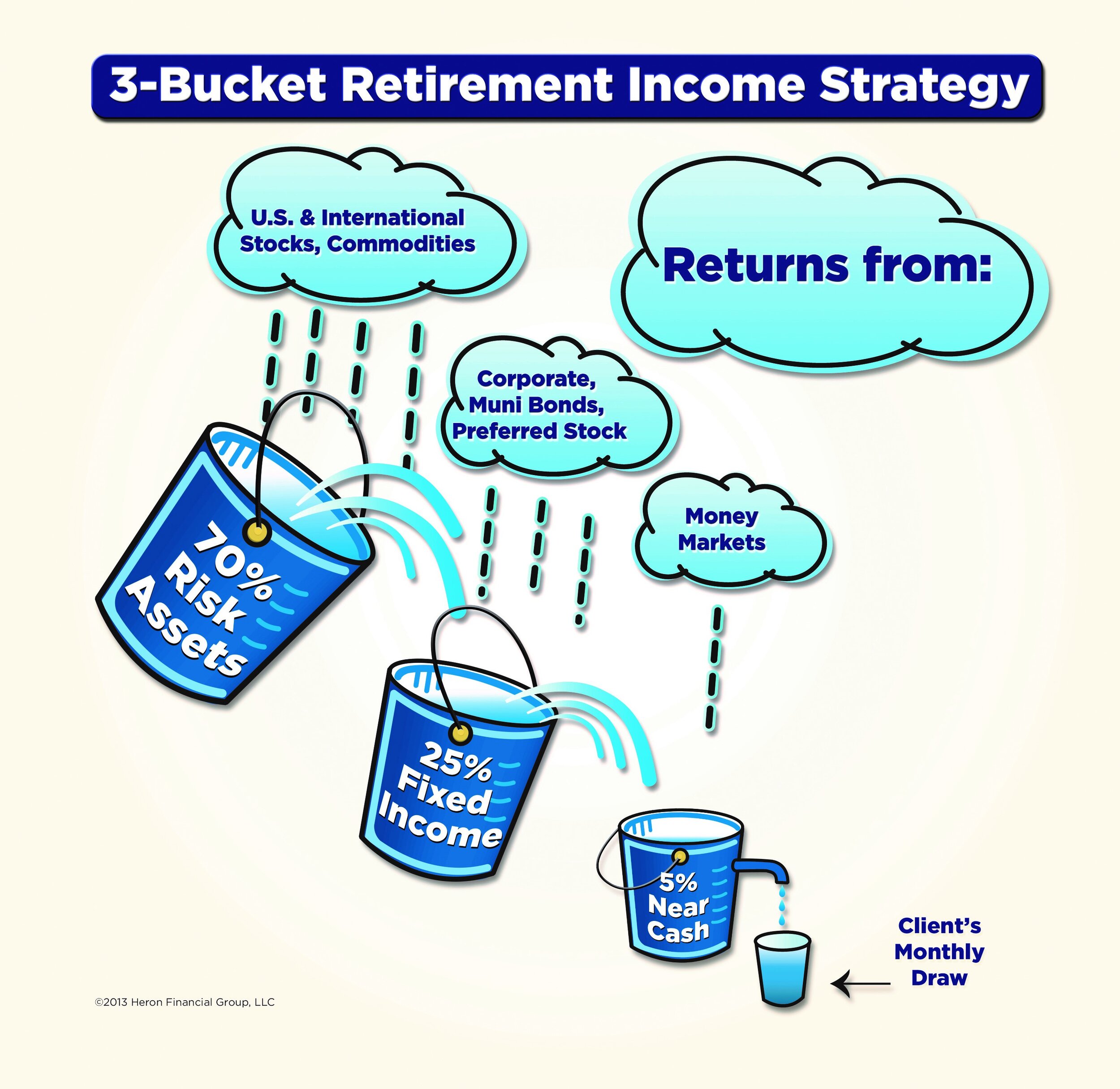

How the Three-Bucket Retirement Income Strategy Works

When a client retires, we split their portfolio into three buckets: Risk Assets, Fixed Income, and Near Cash.

We invest the client’s assets such that the Risk Bucket represents 60-70% of their portfolio, invested in faster growing but volatile US and international equities. We reasonably project that bucket will grow, on average 7-9%/year, but we also know that wide swings in either direction are possible.

Once or twice a year, we rebalance the Risk Bucket to target allocations and pour the excess cash into the Fixed Income Bucket, which contains 25-35% of the overall portfolio. We invest those assets in government bonds & agency bonds, high-grade & high-yield corporate bonds, and preferred stock. We reasonably expect the Fixed Income Bucket to grow 3-4% a year, with far less volatility compared to the Risk Bucket.

Rebalancing the Fixed Income Bucket pours excess funds into the Near Cash bucket, which invests in government securities with maturities of one year or less, commercial paper and CD’s. The Near Cash Bucket generates a negligible return of 0.5-1.5%/year, but with negligible volatility.

Each month, we distribute the client’s Monthly Draw from the Near Cash bucket.

What about bear market years like 2008-9, when US stocks plummeted 55% in 6 months?

When stocks fall dramatically, we simply suspend the distributions from the Risk Bucket to the Fixed Income Bucket, but continue flowing funds from Fixed Income to Near Cash. We DON’T shift funds upstream to the Risk Bucket from Fixed Income and Cash, nor do we aggressively liquidate equities to raise cash.

Why not? We know from history that even in the worst circumstances, equity markets rarely take more than five years to recover to new highs.

The “Black Friday” market crash of September 1929 provides one exception in past 100 years - the DJIA took 25 years to make a new high in 1954. Taking into account the high dividend yields of the 1930’s, however, which peaked at an average 14%/year, an investor who bought stocks right before the crash would have recovered his or her entire investment by late 1936, 7 years from the 1929 peak and 4 ½ years off the market low of summer 1932.

Prior to the Great Recession of 2008-9, the S&P 500 peaked in October 2007, but made new highs by February 2013.

Stocks peaked in January 2020, fell 35% as the COVID-19 pandemic spread but reached new highs in only six months.

There’s nothing magical about the Three-Bucket Retirement Income Strategy. Keeping a year of living expenses in the Near Cash Bucket, and four years of cash flow in the Fixed Income Bucket means that clients can outlast a five-year drought in equity returns.

Good advisors have promoted this strategy for decades. Successfully using the strategy requires only two commitments on the client’s part:

1. Set — and adhere to — pre-retirement savings goals. For the Three-Bucket Strategy to work, the client must amass a large enough portfolio.

2. Live on a 4-5% annual draw. Exceeding 5%/year raises the odds of not having enough funds, net of draw, to sustain future draws after a prolonged downturn in stocks.

David Edwards is president and wealth advisor with Heron Wealth, a $500 million registered investment advisor based in New York City working with 225 client families across the U.S. and around the world. Dustin Lowman contributed additional research for this column.